AI’s Hidden White Space Across Human Work

AI is everywhere yet still early. New MIT research shows 92% of AI tools focus on “thinking” tasks, while just 1.6% of activities capture 60% of AI’s market value.

AI is everywhere — and yet, according to new research, it's barely scratched the surface of where it could go.

The promise of artificial intelligence reshaping the way we work has been discussed so widely that it can feel abstract. You hear that AI will transform industries, eliminate jobs, create new ones, and rewire entire economies. But ask a more grounded question — where specifically can AI be used, and where is it actually being used today? — and the answers get surprisingly precise.

A landmark research paper from MIT's Center for Collective Intelligence, published in March 2026, set out to answer exactly this. The team built a comprehensive "deep ontology" of work activities, disaggregated roughly 20,000 tasks from the US Department of Labor's O*NET occupational database into more than 39,000 granular activities, then mapped 13,275 AI software applications and 20.8 million robotic systems onto that taxonomy. What emerged is the most detailed map yet of where AI is operating in the world of work — and where vast, largely untouched territory still remains.

AI Is, Above All Else, a Thinking Tool

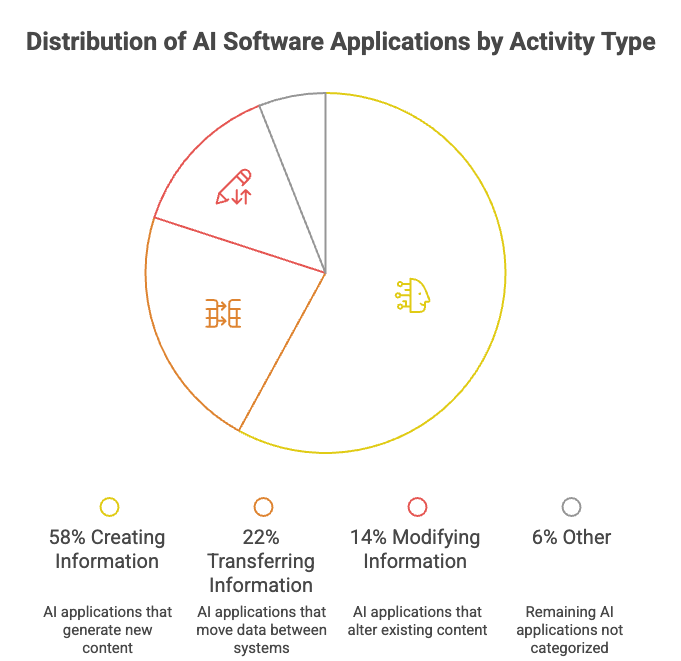

When researchers classified AI software applications by the types of work they support, one pattern dominated: roughly 92% of all AI software applications fall under activities classified as "Act on information" — or what the researchers call "Think."

In other words, the overwhelming majority of today's AI is cognitive AI. It reasons, generates, writes, analyzes, and synthesizes — it doesn't primarily weld, assemble, or navigate physical spaces. Within this "Think" category, three activity types claim the largest share: creating information (58% of AI applications), transferring information (22%), and modifying information (14%).

This maps neatly onto the generative AI era we're living through. The tools most people use daily — large language models, image generators, coding assistants, video creators — are all, at their core, information creation engines. The top individual activities where AI software is most concentrated include "Generate image using computer" (7.18%), "Create content" (3.53%), "Create video" (2.69%), "Answer question" (2.59%), and "Write content" (1.89%). Taken together, just 20 activities account for more than 35% of all AI applications in existence.

This concentration is not incidental. It reflects where AI techniques — particularly large-scale deep learning and transformer architectures — have reached the point of commercial viability. These are the activities where AI is both technically capable and economically justified.

The Stark Reality: 1.6% of Activities Hold 60% of AI's Market Value

Perhaps the most striking finding in the MIT research is just how concentrated AI's economic weight really is. When the researchers combined AI software applications and robotic systems and mapped the estimated market value of all these systems to the activities they support, the top 1.6% of activities account for over 60% of total AI market value.

The distribution is deeply skewed. A small cluster of information-intensive, cognitively rich activities — content generation, information transfer, analysis, code development — attract the lion's share of AI investment and deployment. The vast majority of activities across the human work landscape remain sparsely populated by AI tools, or have none at all.

This isn't necessarily a flaw in AI development. It's a natural reflection of where technical breakthroughs have occurred and where economic demand has been strongest. But it does mean something important for any organization thinking about AI adoption: the activities where AI is most valuable are not evenly distributed, and knowing which activities your business relies on is the first step to understanding where AI can actually help you.

Robots Do; Software Thinks

The research makes a sharp distinction between AI software applications and robotic systems, and the contrast between the two is illuminating.

While software AI overwhelmingly supports cognitive "Think" activities, robotic systems live in the physical world. An extraordinary 89% of all robot deployments fall under "Act on physical objects" ("Do") activities. The dominant single activity? Cleaning floors — which accounts for 76.7% of all robot installations in 2024, largely due to the mass deployment of low-cost consumer floor-cleaning robots.

Remove floor-cleaning robots from the analysis, and the picture becomes more nuanced: physical "Do" activities account for 55% of robotic deployments, while interactive "Interact" activities (like guiding people in public spaces, providing companionship, or teaching) claim 45%. Robots are increasingly stepping into socially embedded roles, not just manufacturing ones.

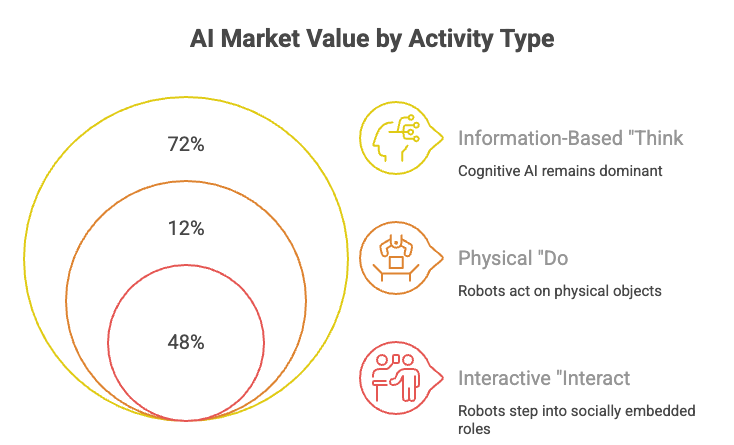

When you combine AI software and robotics into a unified market view, the full picture of today's AI economy comes into focus: 72% of AI's total estimated market value comes from information-based "Think" activities, 12% from physical "Do" activities, and 48% from "Interact" activities (with significant overlap, as interaction often involves information transfer). AI is fundamentally reshaping how knowledge work gets done — the physical and interactive dimensions are growing, but cognitive AI remains the dominant economic force.

The Generative AI Inflection: 2022 Changed Everything

Looking at AI application growth over the past decade, the MIT data reveals a clear and dramatic inflection point.

From 2016 to 2022, AI software applications grew gradually — from just 11 recorded tools in 2016 to 629 by 2021. Coverage of work activities in the researchers' taxonomy expanded to around 2.4% of all activities by that year. Growth was real but incremental.

Then the bottom fell out of the old normal. After 2022, the number of AI applications surged from 1,755 to 7,642 in 2023, and to 12,399 in 2024. The rise of large language models and generative AI triggered a rapid proliferation of tools targeting informational activities. Yet here's what's counterintuitive: coverage of work activities in the ontology expanded only by a factor of 1.2x during this same period, even as the number of applications grew 6x.

What this tells us is that post-2022 AI growth has been deep, not wide. More and more AI tools are being built for the same narrow band of already-popular activities, rather than colonizing genuinely new territory across the work landscape. The explosion in generative AI has intensified competition within a small set of high-value activity categories — rather than expanding AI's reach across the broader map of human work.

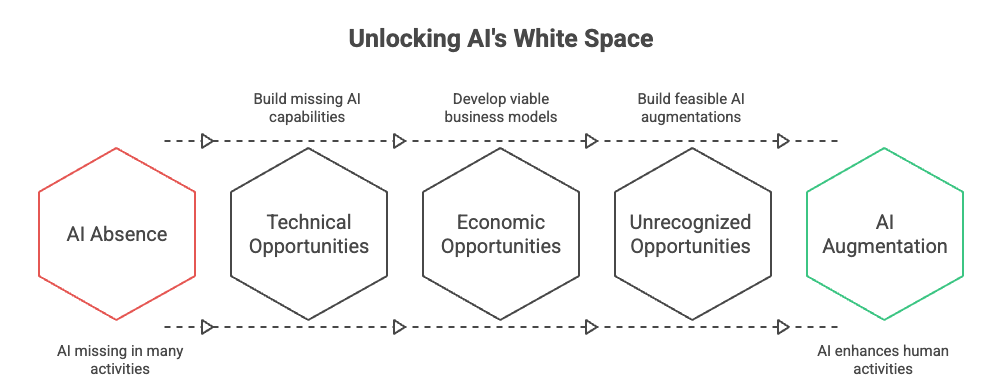

The White Space: Where AI Isn't Being Used Yet

This is where the research becomes most interesting for anyone trying to think ahead.

Because the ontology maps all work activities — not just those where AI has arrived — it also shows clearly where AI is absent. Dozens of "Think" and "Interact" activities show zero recorded AI applications. Activities like "Administer (treat)," "Collaborate (Actor)," "Comply," "Authorize," and "Analyze (Physical Object)" have no current AI tools associated with them.

The researchers argue this is not random. These underrepresented activities tend to share certain characteristics: they are highly context-dependent, socially embedded, physically situated, or require human qualities like empathy, presence, accountability, and judgment — what one referenced framework calls the EPOCH capabilities. They also often involve authoritative or directive roles where human accountability is non-negotiable.

But the gap between technically possible and currently available is not the same as permanently impossible. The researchers identify three distinct types of opportunity in these white spaces. First, technical opportunities — areas where the AI capability simply doesn't exist yet but could be built. Second, economic opportunities — areas where the capability exists but the business model to deploy it hasn't been cracked. Third, and perhaps most compelling, unrecognized opportunities — activities that are both technically and economically feasible for AI augmentation, but that no one has built for yet.

This last category, the researchers suggest, may be among the most valuable entrepreneurial territory in AI today.

What This Means for Businesses Right Now

For organizations navigating AI adoption, the MIT ontology offers something genuinely useful: a structured way to ask not just "should we use AI?" but "which of our specific activities are most ready for AI augmentation — and which ones aren't?"

This shift in framing — from AI as a general-purpose technology to AI as something with a measurable, activity-specific applicability profile — is one that practitioners are increasingly embracing. Organizations working at the intersection of AI strategy and implementation, like AIXccelerate, have found that this kind of structured mapping of work activities is precisely where meaningful AI deployment begins: identifying which tasks within a workflow have strong AI applicability today, which sit in developing territory, and which genuinely still require human depth.

The research underscores that AI's reach is both broader and narrower than popular perception suggests. Broader, in that 13,275 software tools now touch activities spanning strategy, content, analysis, communication, and customer interaction. Narrower, in that the enormous economic weight of AI is concentrated in a remarkably small slice of those activities.

The Map Is Not Yet Complete

The most honest takeaway from this research is that we are genuinely early. AI currently touches fewer than 9% of the activities in this comprehensive taxonomy of human work. The activities it dominates are information-intensive and cognitively rich. The activities it has yet to reach are often socially complex, physically embodied, or organizationally authoritative.

But the trajectory is unmistakable. In 2016, 11 AI tools covered 0.2% of work activities. Today, more than 13,000 cover roughly 9%. The map of where AI can be used is filling in — unevenly, but relentlessly.

Understanding that map — where the current density is, where the white space is, and why — is no longer just an academic exercise. It is core strategic intelligence for any organization that wants to deploy AI where it genuinely adds value, avoid investing in areas where it isn't ready, and stay ahead of where the frontier is moving next.

The question "where can AI be used?" now has a more detailed answer than it ever has. And the organizations that learn to read that map will be better positioned than those still treating AI as an undifferentiated wave washing over everything equally.

Based on findings from: "Where can AI be used? Insights from a deep ontology of work activities" — Cai, YeckehZaare, Sun, Charisi, Wang, Imran, Laubacher, Prakash, and Malone (MIT Center for Collective Intelligence / Sloan School of Management, arXiv:2603.20619, March 2026).